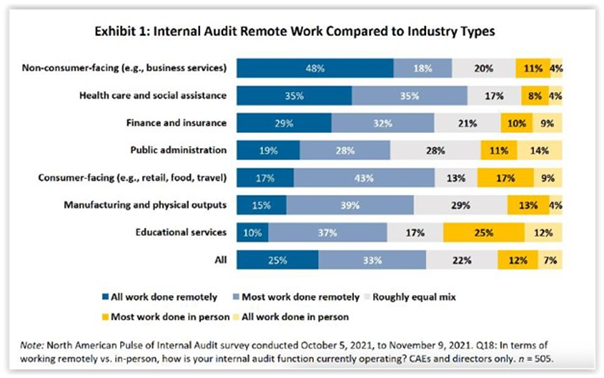

“The Remote Auditor” from the Internal Audit Foundation and AuditBoard reports on the results of recent surveys aimed at understanding the prevalence and implications of the COVID-prompted remote work phenomenon on the internal audit (IA) function. Not surprisingly, the majority of chief audit executives affirmed that their audit teams are primarily or exclusively working remotely; however, the results vary quite significantly by industry, as shown here:

The report surmises that while some IA functions may revert to a fully in-person model post-pandemic, this is unlikely to become (or return to) the norm based on the anticipated permanent shift in how work gets done, with many companies no longer envisioning all employees (including both internal audit teams and their company clients) being in an office/work site five days/week.

The report surmises that while some IA functions may revert to a fully in-person model post-pandemic, this is unlikely to become (or return to) the norm based on the anticipated permanent shift in how work gets done, with many companies no longer envisioning all employees (including both internal audit teams and their company clients) being in an office/work site five days/week.

Internal audit respondents to recent surveys and polls reveal relationship-building and maintenance with non-audit personnel as the most significant challenge by a wide margin associated with remote work. Given the importance of strong relationships to successful internal audits, this is a key concern. Among other helpful tips, the report shares ways in which internal audit executives are seeking to overcome the risks of remote work-prompted disengagement with internal stakeholders.

Access additional resources on our Internal Audit page.

This post first appeared in the weekly Society Alert!