ISS announced today the results of its annual Benchmark Policy Survey for the 2025 proxy season. There were 325 responses to the survey consisting of 199 responses from investors or investor-affiliated organizations and 126 responses from non-investors, which consisted of public companies, public company board members, public company advisors, and other non-investors. The number of respondents varied by question.

The Society submitted a comment letter but did not complete the online survey due largely to the limitations imposed by and concerns about the prepopulated, multiple choice answer selections, which were addressed in the letter.

Key takeaways from the online survey on the topics the Society addressed in its letter include:

US Market-Specific Questions

Poison Pills (Questions 8 – 14)

Survey Question: In the view of your organization, is the adoption by a board of a short-term poison pill to defend against an activist campaign acceptable?

· More than half of 178 investor respondents (52%) said “generally, no,” whereas most of the 88 non-investor respondents (65%) said “generally, yes.”

Survey Question: Should pre-revenue or other early-stage companies be entitled to greater leeway than mature companies when it comes to the adoption of a short-term poison pill?

· More than half of 177 investor respondents (52%) and a plurality of 79 non-investor respondents (43%) said “Yes, but only if their governance structures and practices ensure accountability to shareholders."

Survey Question: Is it ever acceptable for a board to set the trigger of a short-term poison pill below 15 percent?

· A plurality of 173 investor respondents (39%) said “no,” while a plurality of non-investor respondents (38%) said “Yes, the trigger level should be at board's discretion.”

Survey Question: Some companies have adopted a two-tier trigger threshold, with a higher trigger for passive investors (13G filers). Do you consider this to be a mitigating factor for a low trigger?

· Nearly half (and a plurality) of 169 investor respondents (49%) said “No, all investors can be harmed when a company erects defenses against activist investors whose campaigns can create value, so the lowest trigger is the relevant data point,” whereas 78% of 76 non-investor respondents said “Yes, it should prevent the pill from being triggered by a passive asset manager who has no intention of exercising control.”

Survey Question: How important is it that a poison pill include a "qualifying offer clause," giving shareholders the ability to bypass the pill in the event of an offer that is deemed beneficial?

· A majority of 159 investor respondents (59%) said “Important - poison pills should always have a qualifying offer clause to prevent them from being used as an entrenchment mechanism ,” while 52% of 73 non-investor respondents said “Sometimes important - it depends on the trigger threshold and other terms of the pill.”

Executive Compensation (Questions 15 – 24)

Survey Question: Do you consider that ISS' qualitative review in the context of a pay-for-performance misalignment should:

· A plurality of 174 investor respondents (43%) said ISS should “continue with the current approach, which considers a predominance of time-based equity awards to be a negative factor, irrespective of if such awards have extended vesting periods (i.e. longer than four years),” compared to 70% of 96 non-investor respondents who said ISS should “revise the current approach, whereby time-based equity awards with extended vesting periods are considered a positive mitigating factor, similar to performance-based awards.”

For those who responded that ISS should revise the current approach, 66% of investor respondents and 58% of non-investor respondents said time-based equity awards should vest over at least five (5) years for ISS to view such awards as a positive mitigating factor in the context of a pay-for-performance misalignment.

Survey Question: Should a meaningful post-vesting holding period be required for ISS to view such awards as a positive mitigating factor in the context of a pay-for-performance misalignment?

· Most of the 155 investor respondents (68%) said “Yes, a post-vesting holding period requirement should be applicable” and a vast majority of 90 non-investor respondents (73%) said “No, a post-vesting holding period requirement is not necessary.”

Survey Question: Does your organization believe that largely discretionary annual incentive programs, such as those adopted by some large financial sector companies, are problematic, even if the program structure is consistent with industry and/or peer practice?

· More than half of 177 investor respondents (52%) said “Yes, largely discretionary annual incentive programs are problematic, and companies should primarily utilize preset goals and limit the impact of discretion.” A plurality of 93 non-investor respondents (38%) said “No, discretionary programs are not problematic when the structure is consistent with industry and/or peer practice, and the company discloses the main factors considered,” while 31% said “Sometimes, discretionary programs are only problematic if pay is not aligned with company performance.”

Global Environmental & Social Questions

Scope 3 (Questions 33 – 35)

Survey Question: As a stakeholder, does your organization believe that Scope 3 GHG emission reduction targets should be disclosed?

· A plurality of 193 investor respondents said “Yes, companies should be setting targets for their Scope 3 emissions,” while 61% of 101 non-investor respondents said “No, companies should not be required to set targets for their Scope 3 emissions.”

Of those responding “yes,” a majority of both investor and non-investor respondents (131 and 32 respondents, respectively) indicated that the targets should be both mid-term and net zero Scope 3 targets.

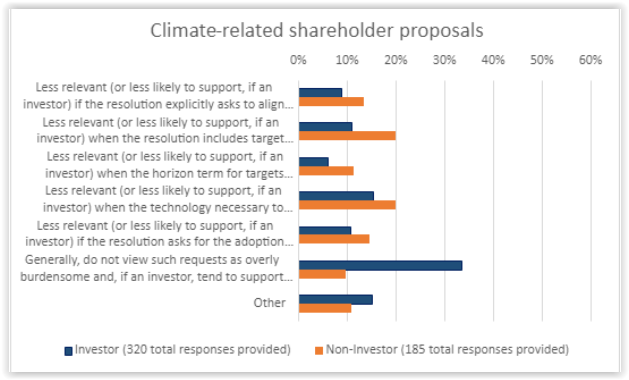

Climate-related Shareholder Proposal (Question 36)

Survey Question: As a market participant, which - if any - of these factors would your organization consider most relevant when addressing proposals asking for a report on or to take climate-related actions. Please select the one(s) that most reflect your organization views.

· A plurality (33%) of 187 investor respondents said they generally do not view such requests as overly burdensome and tend to support them if shortcomings are identified in the company's current approach. The most common non-investor responses (n=79) were split at 20% each: “Less relevant when the resolution includes target requirements for supply chain emissions (Scope 3) and “Less relevant when the technology necessary to achieve full value chain net-zero goals is not yet cost-competitive.” Additional responses are shown below.

Workforce Diversity (Question 38)

Survey Question: Which - if any- of the following human capital management metrics or disclosure topics do you consider that investors should support if requested in a shareholder proposal assuming they are related to markets where such metrics are legal and reflective of societal norms? If more than three, please select your organization's top three (3) options.

· Among 184 investor respondents, the top three choices were “Racial/Ethnic Diversity and Gender Representation Data for different categories of positions across an organization (such as EEO-1 data in the U.S.)” (22%); “board oversight of the human capital management issue raised in the proposal” (19%); and "Adjusted (accounting for factors such as job role, education, and experience) Gender Pay Gap Disclosure" (14%). Among 65 non-investor respondents, the top three choices were “management oversight of the human capital management issued raised in the proposal” (25%); “Racial/Ethnic Diversity and Gender Representation Data for different categories of positions across an organization (such as EEO-1 data in the U.S.)” (20%)' and “board oversight of the human capital management issue raised in the proposal” (20%).

The Annual Policy Survey is part of ISS's annual policy development process. ISS will release key draft policy updates for public comment and release final policies in late November or early December applicable to shareholder meetings occurring on or after February 1, 2025.

See ISS’s release and additional information & resources on our Proxy Advisors page.