The Internal Audit Foundation released its “2026 North American Pulse of Internal Audit” report based on its late 2025 survey of 373 internal audit leaders (i.e., highest-ranking internal auditor within each organization, hereinafter Chief Audit Executive, or CAE) across organization types and industries. Respondents were primarily US-based companies (84%), with the balance representing Canada (13%) and the Caribbean (3%).

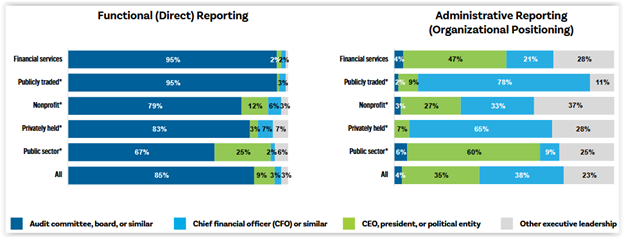

Consistent with recommended best practice, most CAEs have a direct / functional reporting relationship with the board, most commonly, the audit committee, while administrative reporting practices vary fairly considerably by and across organization types, as shown here:

Functional reporting means oversight of the responsibilities of the internal audit function, including approval of the internal audit charter, the audit plan, evaluation of the CAE, and compensation for the CAE, while administrative reporting refers to oversight of day-to-day matters, expense approval, human resource administration, communication, internal policies, and procedures.

The report includes an abundance of benchmarking data on the internal audit function budget, staffing, audit plans, CAE responsibilities, and CAE reporting relationships.